Can we deposit donations received in foreign currency from NRIs in cash or by cheque from a foreign bank in normal account of NGO or it has to be deposited in FCRA account only? Please advise.

Thanks.

V.K.Kalsi

Can we deposit donations received in foreign currency from NRIs in cash or by cheque from a foreign bank in normal account of NGO or it has to be deposited in FCRA account only? Please advise.

Thanks.

V.K.Kalsi

Dear sir,

The NGOs are exempted from PF coverage till 31st March, 2015, a notification was published on 14 May 2010 by Ministry of Labour and Employment. Notification is attached here with for ready reference. After that there is no news if this exemption is extended for any period.

It is very important that many NGO were taking benefit of this notification now the question comes that these NGOs have to register with PF department ? or should wait for extension of notification? click here for PF notification

Arvind Kumar

Is there any rule under FCRA Act which prohibit relatives to be the part of an Executive Board Committee of an NGO/Society/ Charitable Organisation/ Trust. Am looking for details in this regard.

Ambreen Khan (Ms.)

Dear Members,

We (Nettur technical training foundation) is a registered not for profit organisation registered with Income tax commissioners and covered under section 11 and 12 of the IT act.

With respect to our assessment we have different views taken by different assessing officers.

As per the act we presume that 85% of the gross receipts should be spent on capital and revenue expenses to avail full exemption in a financial year.

The subject is rather leading to confusion year after year.

Kindly give your opinion and views.

Regards

Louis

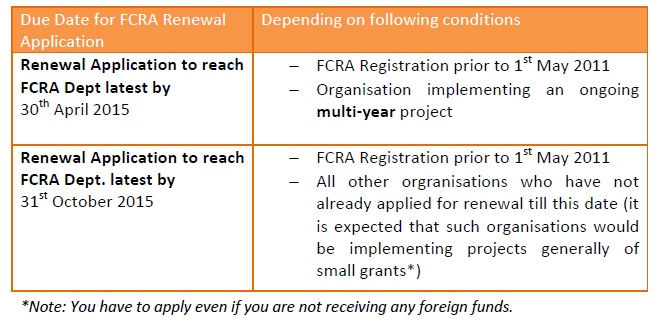

As intimated earlier through SRRF Dialogue, FCRA renewal for certain FCRA registered organisations are due, a Table is given below to help identify Due Date for renewals.

Although when the FCRA Act was made effective, FCRA Dept had explained that the application would need to be submitted online, however since the Dept has not put this application online, it is suggested that based on above dates FCRA Renewal application should be submitted.

Although when the FCRA Act was made effective, FCRA Dept had explained that the application would need to be submitted online, however since the Dept has not put this application online, it is suggested that based on above dates FCRA Renewal application should be submitted.

PROCEDURE:

SRRF has a Helpline to help organisations who face problems in applying. Helpline No. is 9350184168.

_____________________________________

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place, New Delhi – 110008

e-mail: socio-research@sma.net.in; website: http://www.srr-foundation.org

Hello,

My name is Uma and I am writing on behalf of an educational NGO based in Chennai. We have been operational since 2007 and we are providing Montessori education to the under priviledged children by adopting the local balwadis.

As we are looking to expand, we are looking for external resources for funding and the first question which comes up is the registration certificate. The trustees of this organization executed the trust deed on non-judicial stamp paper and we do have the copy of the trust deed. We are also registered under the section 12AA of income Tax and getting 80G exemption as well since 2008.

Now we applied for the FCRA application and the lawyer is saying that the trust is not registered and asking for the registration certificate.

1. Is execution of the trust deed on stamp paper not considered as registration ?

2. What is the registration certificate ? how do I find this ?

3. If we need to do the registration, will our history of the work be considered for evaluation ?

4. Is there a way to find out whether our trust is registered ? if so, where ?

Can somebody provide a clarification on this ?

Sincerely,

Uma

Nishkam Chennai

Dear Members,

Does the allocated fund to CSR lapses in case the organization could not spend in the year. If no than, can it be used for next year. Under which Government order this is clarified?

Looking forward to your support.

Thanks,

Dear Friends,

Under the provisions of the FCRA 2010, any change in the Board members in excess of 50% shall be made with prior permission. This does not technically apply to organizations registered prior to 27th December 1996 as there was no declaration signed by the organization this effect while applying for registration.

The query/doubt that I have is that the prior approval for the nomination of Board members is to be sought when the 50% change occurs “over a period of time” or “at any given point in time”.

Thanks and regards,

—

B V Soma Sastry

In a decision by Income Tax Appellate Tribunal (ITAT), Mumbai it has been held that a Trust whose objects include ‘international welfare’ is a charitable entity and cannot be denied S.12A registration.

DIT (E) who rejected the application for S.12A registration of the Trust in its order had contended that Critical Art & Media Practice’s (to be referred as Trust) objects include charitable as well as non charitable activities, such as hosting of artists-in-residence programmes for international artists and raising funds for organizing trips, seminars and conferences within and outside the country. Considering S.11 applies only for income to be applied for charitable purposes within India, the Trust cannot be given the tax exemption status.

The trust filed an appeal before ITAT (Mumbai) against the Order. The Tribunal divided the issue into two parts, one for examination of charitable activity and second applicability of tax exemption (S.11) on the same. It after examining the case, held that while it is true that the objects of the Trust are such that it may apply some of its income outside India, however the test of an entity being charitable has to be based on definition of ‘charitable purpose’ under S. 2(15). It stated that this definition nowhere states that any activity undertaken by a Trust outside India is not a charitable activity. Thus even if an entity applies its income on welfare activities outside India, its charitable purpose needs to be seen in light of definition given under S.2(15).

It further stated that in case the Trust applies its income on objects which are outside India and if not authorized by CBDT that expenditure would not fall within the definition of application of income under S.11 and would need to be dealt accordingly.

___________________________________

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place, New Delhi – 110008

e-mail: socio-research@sma.net.in