- Treatment of sale proceeds assets out of FCRA fund

Good Afternoon,

I seek your valuable advice for the following.

Old assets bought out of FCRA project in 2017 has been sold to ordinary local buyers in town. Where should we deposit the money/ cheque given by them?

Can cheque be deposited in either FCRA utility bank account or SBI MAIN Branch?

Anurita

Guwahati,

Assam, India - Latest Amendments in FCRA Rules & Forms – 3

These amendmentshave been brought to further tighten the rules and reporting Forms. The changes are applicable from the date of publication in the Gazette.

In earlier two posts, following topics have been covered:

- Key Functionaries and applicability of FCRA towards For-Profit entities

- Project-wise disclosure of Purpose&GeographicalAreas where projects are being implemented

In today’s posts we cover issues relating to

- Prohibiting foreign citizens as Board members / trustees, and

- FC to be used in India only.

Eligibility of Foreign citizens as Key Functionaries

- As a practice, FCRA Dept did not allow foreign citizens as Key Functionaries, though this was not specified anywhere in Act or Rules. FAQs did mention it, but considering FAQs do not have legal sanctity, the rule remained more of a practice and not a legislative provision.

- For first time, FCRA Dept has made it part of FCRA Rules 2011. Explanation 1 under Rule 9(5), has made it quite clear, that foreign nationals, other those of Indian origin (i.e. OCI card holder), shall not be considered eligible for grant of FCRA registration.

- However, the term used is ‘shall ordinarily not be considered eligible‘. This means, that scope exists for allowing such persons to be considered as key functionaries on case-to-case basis.

FC to be used for activities in India

- Under the same Rule [i.e. 9(5)], it has been clarified that the Foreign Contribution (FC) shall be utilized only for activities carried out in India. However, it has been added that this contribution should be on such activities which are in accordance with the association’s stated objectives and for the purposes for which it has been received.

- The term ‘activities carried out in India’ has created a number of doubts. Normally this term has been interpreted in accordance with S. 11(1) of Income Tax Act 1961, which states ‘…….to the extent to which such income is applied to such purposes in India….’. ‘Purposes’ has generally been interpreted as applied to objects, where benefit is received in India. Would activities carried out in India would mean that FC can be applied only for activities in India. For example, would NPO officials travelling abroad to attend meetings / make presentations, which ultimately help NPO create awareness about projects being implemented in India, would be treated as activities carried out outside India or would any activity which benefits Indian objectives would be considered as being carried out in India. This term is likely to cause a lot of heartburn as interpretations are likely to vary.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Latest Amendments in FCRA Rules & Forms – 2

This amendment has been brought to further tighten the rules and reporting Forms. The changes are applicable from the date of publication in the Gazette.

In yesterday’s post, topics of Key Functionaries and applicability of FCRA towards For-Profit entities were covered.

In today’s post, issue relating to Project-wise disclosure of Purpose & Geographical Areas where projects are being implemented is being covered.

Purpose

- Govt has come out with a detailed schedule of 105 predefined categories covering Religious (16), Cultural (18), Economic (19), Educational (22), Social (30). A NPO desirous of registration under FCRA would need to select one or more of them in its application.

- The purpose as selected in its application would be specified in the FCRA registration certificate. Even current FCRA registered entities would need to comply with this requirement, within oneyear.

- In effect, above means, that if a NPO’s activities as covered in grants do not get covered within the purpose / activity specified in its registration certificate. It will need to apply for amendment. For this purpose, Govt has formulated a Form FC-6F. This will become quite an onerous responsibility, and in case delays are experienced as generally is the trend at FCRA, a major bottleneck.

Geographical Area

- Similar to as mentioned under Purpose above, all NPOs would need to ensure that the State in which they plan to undertake activity is mentioned in their Registration Certificate.

- A fee of Rs 300/- per state has been affixed for the same.

Consequences of above requirements

- Concern is, would this become a basis for some form of objection or even penalty, if the state covered in the FCRA Registration certificate is not included in the byelaws of the NPO.

- Please note ensuring geographical location in FCRA registered entity is important, since this information is also being sought in Annual Return (FC4), when Project-wise information (para 3(a)) and location of assets (para 3(ba)) & 3(bb)) is being asked for.

- Proposed Rule 17B (3) gives right to Govt to reject or approve the application after undertaking such inquiry as it deems fit.

- It is foreseen that this could become a basis of number of disputes and penal provisions by the Dept.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Latest Amendments in FCRA Rules & Forms -1

This amendment has been brought to further tighten the rules and reporting Forms. The changes are applicable from the date of publication in the Gazette. Considering large number of amendments which impact several aspect of FCRA legislation, it is decided to cover various amendments through a series of posts. So please bear with us. In this post we cover impact of amendments on For-Proft entities.

Key Functionaries defined

- A Key functionary has now been formally defined. It includes Board members, Trustees, Office bearers of governing body (covering Trust, Society, Trade Union, etc). However Chief Functionary is still not defined, although it is the person who signs all documents to be submitted to the FCRA Dept online. Whoever signs application for registration / prior permission automatically becomes Chief Functionary. Subsequent changes, if any are informed to the FCRA Dept formally through Form FC-6E.

- Any other officer or person, by whatever name called, who has control over or responsibility for the management or affairs of such person. Thus, a CEO who is not a director or office bearer of an NPO would now be covered. Earlier say husband of a managing trustee, would largely run the organisation, without formally having a post. Now theoretically such a person would be covered by the definition of ‘Key Functionary’.

- Important pointto note, while For-Profits were covered earlier too, but now definition specifically states that partners in a partnership, Karta of HUF, director in a company will be covered.

The above raises a very interesting point, are For-Profit entities covered under FCRA. Theoretically once the definition of ‘Person’ was introduced through FCRA 2010 Act, For-Profit entities got covered, however how many have heard a For-Profit entity getting FCRA registration. There have been several instances, where FCRA Dept has refused to give FCRA registration on the ground that the applicant is likely to make ‘personal gains’. In fact clause (vi) of S.12(4), says exactly the same and is one of the ground for refusal to granting registration certificate.

I believe emphasis on partners, directors ismainly to discourage NPOs to start incorporating For-Profit entities, to avoid FCRA registration process.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Subscriptions to ZCZP Bonds to be allowed as CSR

Ministry of Corporate Affairs (MCA) has added a new entry (Entry No. xiii) in Sch. VII of the Companies Act 2013, allowing ‘Subscriptions to Zero Coupon Zero Principal (ZCZP) instruments listed on Social Stock segment of various stock exchanges’[1].

[2]The above subscriptions are subjected to following conditions:

- MCA has limited that maximum amount that a company can invest through ZCZP is 10% of the total CSR Expenditure for that FY.

- The NPO can issue ZCZP Bonds for a project, which will not be for a period more than the three years plus year in which introduced.

- At the end of the project, NPO would need to transfer any unspent amount to any of the Sch VII listed funds, thus no need to transfer back unspent funds to the company at the end of the Financial Year.

- Company management is not responsible for giving UC for such a project, that means, subscription amount to such Bonds will be treated as CSR expenditure for reporting by the company.

- Company management is not responsible for monitoring of such projects, presumably as SSE requires such NGOs to submit annual and project-end evaluation reports to SSE portal.

For any further information on above topic, watch out for further post.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008

[1]GSR 416(E) dt 27-5-2026

[2]GSR 415(E) dt 27-5-2026

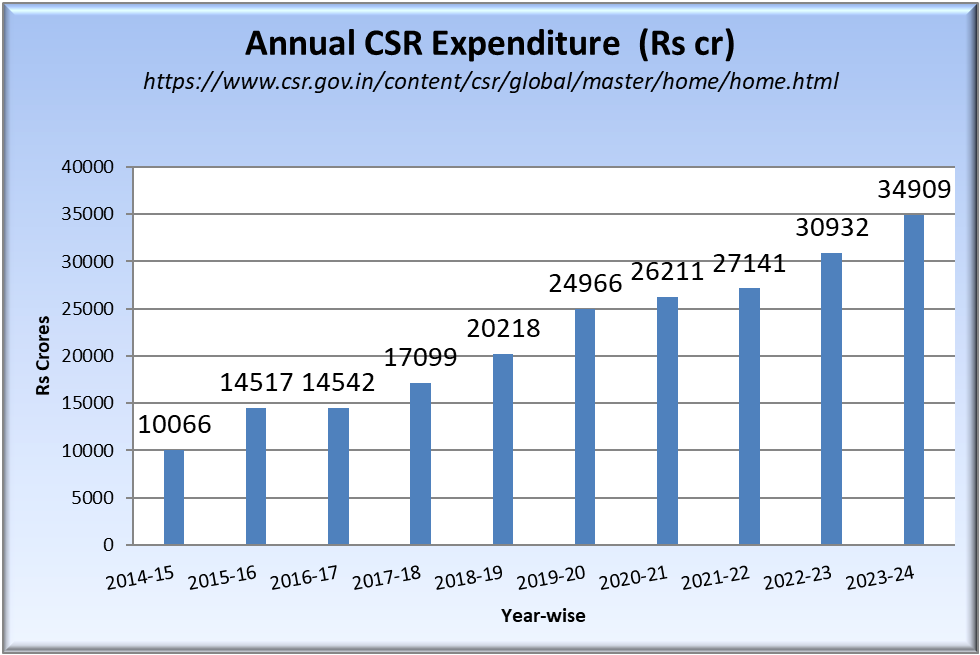

- CSR spending during FY 2025

Listed companies CSR spending during FY 2025 rose by 23% to Rs 22,212 crores compared to Rs 18,011 crores during FY 2024 (source: Indian Express April 20).

Let’s not forget this data is only for listed companies as FY 2024 spending under CSR by all eligible companies was around Rs 35,000 crores. Main reason for increase in CSR is due to large increase in profits of listed companies (one estimate puts it around 22%).

It is noted that annual CSR spending has been increasing by around 27.4% at average annual growth since FY 2014-15, the first year of official CSR introduction.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - FCRA 2026 put on hold

FCRA amendment Act 2026, which was introduced by the Govt on 25 March 2026 in the Parliament. The bill puts in place mechanism of how Govt would takeover the assets and properties of all those entities whose FCRA has been cancelled.

Well now, the Sector can breathe easy, at least there is a temporary relief to these entities, as the Govt has decided to put the amendment bill on hold. The Govt sensing opposition parties getting together and launching major protests, has for the time decided to put the Bill on hold.

The data provided on FCRA website dashboard is indicative of how many NPOs could be impacted if the Bill becomes an Act. The following data is based on today’s data as available on FCRA website:

Nos. % NPOs Active under FCRA 14,965 29% Registration cancelled 21,979 42% Deemed Expired 15,180 29% 52,124 Based on above data, it is so alarming to note that the Govt could potentially take over the assets of 71% of all FCRA registered entities, which have at one time or other registered under FCRA. This would be almost a death knell for the survival of the Sector.

__

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Guidance Note on filing of FCRA Annual Return (FC-4)

Many of SRRF Dialogue members would be involved in finalising their FC4 return. This year’s return has certain issues, which is creating a lot of confusion, amongst most NPOs. SRRF Dialogue is posting a para-wise Guidance to help members fill up their FC4 and comply.

S.No. FC-4 Particulars Comments Para 1 Name Address, FCRA Reg. No. & Date Data is autopopulated from data maintained by FCRA Dept as per FCRA registration. Para 2 Details of FC Receipts (a) Brought forward FC This information needs to be typed and will not be autopopulated based on last year’s FC-4 RECEIPTS (b)(i) Receipt – Intertest This should match with R&P (b)(ii) Other Receipts Generally from sale of assets, etc. (b)(iii) Income Tax refund trfd from non-FCRA Bank A/c This is a new field and needs to be filled in, in case NPO has trfd TDS refund from non-FCRA to FCRA A/c. (c) FC rec’d from foreign source during the FY (i) Directly from a foreign source In most cases FC would be disclosed under this source only. (ii) as transfer from a local source Not likely (d) Total FC (a+b+c) autopopulated (a)+(b)+(c)

Ensure this total agrees with R&P(ii) (a) Donor-wise details of FC rec’d in form of a Table Table has 7 columns, while all others are self-explanatory, col 5 needs special mention. Col 5 requires disclosure of ‘Purpose’ for which grant has been rec’d. This should align with the Purpose as specified in the FCRA registration. Generally Social, Educational or Economical. (ii) (b) Cumulative purpose-wise amount will be Will be autopopulated according to disclosure in previous Table.

Ensure this total agrees with figure Para 2(d) above.Para 3 Details of Utilisation of FC (a) There is amajor problem in this Table, relating to Admin costs. If Admin costs of a project are included under individual project Utilisation costs column, then this will double Admin costs, as the Admin costs are also required to be separately disclosed under (ii) below the Table. Assumption by the Dept seems to be that Admin costs are not part of Project costs, and hence should not be included in the Utilisation cost of a Project.

If one includes Admin costs both under individual projects as well as under (ii) also, then Total costs will become higher than total utilisation under (iii). The Table does not accept it. Hence ideally do not include Admin costs under Utilisation column (8) of Table and disclose it under (ii) only. Problem arises that than unutilised balance under individual projects becomes higher by the amount of Admin costs not included under the projects. To overcome this issue, one needs to reduce Admin costs from FC Receipts under col 6 of the Table.Important: Since the above means that Total Receipts in this Table and as disclosed under Para 2 above do not match, a explaination in the form of reconciliation may be given alsong with Auditor’s Certificate. 3(a)(i) Utilisation for projects as per aims & objectives of the association Data will get autopopulated from Table under 3(a) 3(a)(ii) Total Admin Exps. This figure needs to be typed and should be separately worked out. 3(a)(iii) Total Utilisation of FC This is auto-populated by adding figures in Col 8 under 3(a)(i) & (ii). (b) Give details of all the assets capitalised and also included in Para 3(a) above. (ba) Provide opening balance, additions, disposed and closing balance for each category of asset, as in FCRA Fixed Asset schedule. Ensure figures are matching with what is included in Bal Sheet. In which case the table in FC4, will not cross-tally as the Table does not include dep’n. Some experts are of the opinion, that only Gross Values should be disclosed, but then value does not match with Balance Sheet. Also some NPOs do not carry forward Gross Values, as they carry forward only WDVs. (bb) Give details of Immovable properties @ 31-3-2025. Make sure, values agree with Balance sheet. (c) FC trfd to other associations before 29-9-2020 There is no clarity why this detail is being asked for, since NPOs would not be able to remember all the funds trfd to NPOs before 29-9-2020. What it should state details of funds trfd to NPOs in violation of S.7 during this year. Most likely all will fill Nil. (d) Total utilisation in the year (a+c) This is auto-populated figure adding 4(a)+4(c) 4 Details of unutilised FC 4(i) Total FC invested in FDs One has to give totals of all FDs here as per requirement. Ensure figures are in agreement with your FCRA R&P and FCRA Bal. Sheet. 4(ii) Balance of Unutilised FC, in cash/bank, at the end of the year (a) Cash in Hand (b) FC designated A/c (c) Utilisation Bank A/cs (d) Total (a+b+c) This gets auto-populated by adding above three figures. Please compare this figure with unutilised figure in Table 3(a). These should match, if not go back and look into the reasons for the same. 4(iv) This should read 4(iii), but Form numbers it incorrectly as 4(iv) This is Table for working out carry forward of Admin Exps. A. b/f unspent part of allowable Admin Exps. Since this is the first year, when Admin exps have been allowed to be carried forward, most likely it should be Nil for almost all NPOs. B. Total FC rec’d during the year This is autopopulated, data considers FC rec’d+interest+Other Income under Para 2 above. C. Allowable Admin Exps. Of current FY (20% of B) This is autopopulated by system D. Total Admin Exps. Incurred during the current FY This is autopopulated by system, picking the data from Para 3(a)(ii) E. Admin Exps. Of current FY utilised out of A above. The system is designed, so that it first allows Admin exps to be set-off against b/f unspent balance. However choice is left to NPO F. Admin Exps of current year utilised out of C above Allows NPO to decide how much to utilise against current year’s allowable admin exp. G. Unspent part of C above available to be carried forward This is calculated by system H. Out of G above, amount to be carried forward to next FY Type the amount of Admin Exps. Not utilised out of G I. Reason for carry forward of unspent part allowable Admin Exps. To next FY Give reasons, if some part of Admin Exps. Is being carried forward. Other columns are self-explanatory

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Show Cause Notice under Section 14(1) (e) of FCRA 2010

FCRA Dept has started issuing show-cause notices to registered entities, which have not received FCRA funds in last three years (FY 2021-22 to 2023-24). A sample copy of the Notice issued can be seen here. The Show cause Notice is being issued under S.14(1)(e) of the FCRA 2010 Act. The section is reproduced below:

S.14(1)(e): The Central Govt may, if it is satisfied after making such inquiry as it may deem fit, by an order, cancel the certificate, if the holder of the certificate has not been engaged in any reasonable activity in its chosen field for the benefit of the society for two consecutive years or has become defunct.

If you have rec’d such a Notice, and you wish to continue with your FCRA registration, you will need to write to the FCRA Dept within 21 days from the date of Notice and convince the Dept that you wish to continue with the activities, and are in negotiation / making efforts to receive FCRA donations in near future.If possible, provide some documentary support for the same.

However, ultimately it will be the decision of the FCRA Dept whether it cancels the Notice or accepts your representation.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Delhi HC rejects ‘one line refusal’ of FCRA Dept

Indian Social Action Forum vs Union of India.[1] [WP(C) 10199/2016&CM APPL. 37992/2021 – Delhi HC: Order dt 24-07-2025)

Delhi HC (Justice NitinWasudeo Sambre & Justice Anish Dayal) decided in favour of appellant NGO – INSAF, whose FCRA renewal registration application was rejected by the FCRA Dept. vide its email communication dt 21-10-2016.

In its order the HC stated that it was concerned that the order was without reasons and even the basic considerations. It was only ‘one line email’ stating that the Union of India rejected the prayer of the petitioner for renewal for the period from 2016-2021. Although during the hearing, Union Govt has tried to justify its decision by narrating the reasons in the affidavit. Since the said order cannot be substantiated by these reasons, such conduct of Union of India reflects complete non-application of mind, and therefore can also be termed as in violation of principles of natural justice.

In view thereof the said order cannot be sustainable.

Subsequent affidavit submitted by Union of India, stated that the basis for rejection of renewal is on account of S.12(4)(e) of FCRA Act 2010, where certain criminal prosecution cases were pending against the office bearers. Petitioner informed the Court that in all the cases, the office bearer of the petitioner stood acquitted in all but one case. HC directed Union of India to consider the renewal requestof certificate afresh, within 90 days of the Order, and allowed the petitioner to submit all such material which it considers justifiable for claim of grant of renewal within 30 days. HC specified that it has adhered to the timeline of 90 days in view of the proviso to S.16 of the Act, requiring it to provide its decision and reasons for rejection with 90 days.

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008

https://www.livelaw.in/pdf_upload/74824072025cw101992016160738-612534.pdf

- SC backs Madras HC decision of restoring FCRA Renewal

UNION OF INDIA Versus M/S SHARMA CENTRE FOR HERITAGE EDUCATION, SLP(C)No. 26284-26285/2025[1]

We refer to Madras HC case that we reported only a few days back (https://blog.srr-foundation.org/?p=4788), where Justice N. Anand Venkatesh had decided in favour of appellant NGOs, whose FCRA registration was not renewed by FCRA Dept. HC had quashed the refusal letters of the Dept, and asked the FCRA Dept. to issue renewals.FCRA Dept filed a Special Leave Petition in the SC, requesting to quash the HC Order. Matter was heard by Bench of Justices Vikram Nath & Sandeep Mehta. In a sharp comment to Additional Solicitor General representing Dept, Justice Nathasked

Have they misappropriated? is there any abuse of these funds received by them? There is no such finding at all. If they are doing some social service for the society, what is your problem? You monitor, keep a check, let them file their accounts annually – that’s all. Don’t complicate things, don’t further harass them. Comply with the High Court Order.

Effectively with this decision of SC, the two NPOs which had gone to the court for relief have been granted the relief. It is fervently hoped that more NPOs will pick up the baton and go to the courts for relief and not wait endlessly for FCRA Dept’s mercy.

Dept’s strict attitude while considering NPOs applications, can be seen from the unreasonably high rejection rate, that MHA has published in its Annual Report for FY 2023-24.

Service Total Applications Disposed Approval Granted Rejections No. of Applications Rej. Rate (%) FCRA Renewals 8306 6293 2013 24% FCRA Registrations 2154 1209 945 44% Prior Permission 296 39 257 87% Change of Board Members 8347 4185 4162 50% —

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008

[1]https://www.livelaw.in/top-stories/supreme-court-rejects-union-challenge-to-high-court-order-for-renewal-of-ngo-fcra-registration-304484

- Madras HC quashes refusal to Renew FCRA due to transfer to sister concern

Madras HC quashes refusal to Renew FCRA because funds were transferred from one sister NGO to another without any malafide

Sharma Centre for Heritage Education & Ellen Sharma Memorial Trust vs Union of India &Anr.[1] [CMA No. 746 of 2022 & WP No. 4887 of 2022 – Madras HC: Order dt 27-06-2025)

Madras HC (Justice N. Anand Venkatesh) decided in favour of appellant NGOs, whose FCRA registration was not renewed by FCRA Dept. The denial letter stated that renewal was denied based on S.16(1) read with S.12(4)(a)(vii) of FCRA 2010. The communication did not specify the nature of violation.

FCRA Dept in its response, filed a counter affidavit alleging violation under S.7 of the Act, stating that funds had been transferred among the sister NGOs without prior approval. Dept argued that this violation disqualified the NGOs from receiving renewal.

In its judgement, the HC recorded that the Dept’s communications have not contained any reasons except stating that the renewal was refused under S.16(1)…. Of the Act. Court held that the breach by the parties was minor, as the Dep’s own report delivered to the Court in sealed cover, did not show any material that the two Trusts had misused the FC and that there was no personal gain no diversion of fund for undesirable purposes. The court stated that transfer of funds, without any allegation of mis-proprietary is nothing more than a procedural breach. The Court quashed the FCRA refusals and stated that the petitioners should be granted renewal.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008

- Which account funds to be deposited on sale of FCRA Property

Dear Members,

Require your opinion:If a FCRA certificate holding Society-cum-Trust has obtained permission from the Charity Commissioner to sell its immovable property which was purchased 20 years back from its Foreign funds. Now, the authorized buyer which is a LLP company or a Trust wants to electronically transfer the amount agreed upon.

QUESTIONS:

- Which FC account should the buyer be advised to transfer to: the main account at SBI, NDMB or its FC utilization account (from which the immovable property was purchased)?

Kindly guide us.

Dhruv Mankad

- Renewal of 12A and 80G Registration

Most NPOs were granted their 12A and 80G registration certificate in the year 2021. These certificates are valid for 5 years (in case of Regular or Final Registration) from the date of registration and renewal will in most cases will remain effective till AY 2026-27.

The renewal process must be initiated at least 6 months before expiry of the 5-year registration granted under S.12AB [See S.12A(1)(ac)(vi)].

Thus if your NPO rec’d the 12A registration during FY 21-22 covering AY 22-23, then if it has been valid for 5 years, it will expire at the end of AY 26-27, i.e. 31-3-2026. Hence you need to apply at least 6-months prior to expiry, i.e. before 30th September 2025.

There is some confusion whether 12AB has been extended for 10 years, since section 12A(1)(ac)(vi) now states that renewal is due after 10 years. It is our understanding that extended 10-year validity will apply only prospectively – i.e., after your current term ends, the renewal is likely to be granted for 10 years. Without such express order, an organisation will be taking a risk and hence we strongly recommend that you apply for renewal before 30th September 2025.

Re 80G, present Finance Act 2025 does not have provision of 10 years, and hence will continue on the basis of 5 years.

Finance Act 2025 has already been passed in Lok Sabha and needs to be approved in Rajya Sabha, although being a money Bill it does not require mandatory approval of the Rajya Sabha.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Major Changes for charitable organisations – ITR-7

Recently CBDT has notified most of the ITRs, after making changes, including ITR-7. These changes were notified on 9-5-2025. Major changes are highlighted below:

1. NPOs need to disclose several new information earlier not asked for in their ITR 7

- Capital Gains Segregation Based on Date: As per the amendments introduced in the Finance Act, 2024, a major update has been made to Schedule-Capital Gains in ITR-7. Taxpayers are now required to report capital gains separately for transactions executed before and after July 23, 2024 — the date from which the revised capital gains rules came into force. This change is expected to affect how indexation and tax calculations are carried out.

- Section 24(b) Reporting for Interest on Housing Loans:New fields have been added to capture deductions claimed under Section 24(b), improving disclosure on interest paid for house properties owned by these entities.

- TDS Section Code Inclusion:Entities will now need to specify the TDS section code in the Schedule-TDS to enhance verification of tax deductions.

- Under Para A20 of the ITR-7, details of registration under other laws (such as FCRA, Darpan, etc.) are required to be disclosed.

- Voluntary contributions need to be disclosed between Domestic & Foreign, and under these broad division between Corpus & others. In case of Foreign Contribution (FC), one would also need to disclose purpose for which FC has been received.

2. Due Dates for filing of ITR 7

- For NPOs, including companies, required to undertake audit of their accounts, the due date remains the same as earlier, i.e. 31st October 2025.

- For NPOs not required to undertake audit of their accounts, normally due date is 31st July, however this year it has been postponed to 15th September 2025.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Deadline for filing Form 49C extended

Foreign companies with Liaison offices, which till last year were required to file Form 49C within 60 days from year-end can now file the same in eight months from the year-end, i.e. by 30th November. This has been done vide Income Tax (4th amendment) Rules 2025. This extension provides additional time for LOs to gather and report accurate financial and operational details, aligning the compliance timeline more closely with other regulatory requirements. The amendment came into effect from the date of its publication in the Official Gazette. This is effective from the date of publication in the Gazette, i.e. 9-2-2025.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Recent Amendments in FCRA Forms (Notification GSR 342E dt 26-05-2025)

This amendment has been brought to bring into rules (through Notification) various changes brought in by FCRA Dept through a Checklist brought in by FCRA Dept for submitting various documents at the time of applying for registration.

Important ones are briefly summarized below.

Form FC3A (for registration amended)

- Last three years financial statements [Balance Sheet (B/S), Income & Expenditure (I&E) & Receipt & Payment (R&P)] and audit reports to be submitted along with the registration application. Earlier form did not specify this requirement.

- Year-wise activity reports for three years.

- I&E & R&P should reflect project/activity-wise expenditure. These statements should reconcile with each activity in the activity-wise report. If not, then submit a CA certificate giving such details and ensuring figures as per activity reports reconcile with the relevant I&E & R&P.

- Proforma affidavit format amended. It now requires each Board member to confirm that s/he is an Indian citizen, give OCI Card particulars if applicable, no conviction or prosecution pending.

- If NPO involved in publication related activities or if the Objects include such activities, then Chief Functionary needs to give an undertaking that no violation of S.3(1)(g) – reproduced below for ready reference

No FC to be accepted by association or company engaged in the production or broadcast of audio news or audio visual news or current affairs programmes through any electronic mode, or any other electronic form as defined in clause 2(1)(r) of the Information Technology Act 2000 or any other mode of mass communication.

- If any publication of NPO registered with Registrar of Newspaper for India (RNI, then obtain a certificate from TNI that it is not a Newspaper.

Form FC3B (Prior Permission) &FC3C (for renewal amended)

- Similar changes made in above forms, particularly relating to Proforma format.

Form FC4 (Annual Return)

- Purchase of new assets a Table has been added, requiring details of assets purchased.

- Details regarding movable & immovable assets, new Tables provided, requiring that figures should match with details in Balance Sheet.

- Chartered Accountants now are required to include in their own certificate project-wise opening & closing balances, alongwith project-wise receipt & utilization. This is quite onerous responsibility and will require Cas to spend substantial time in ensuring these figures.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Difficulty in FC-4 return filing for FY 2024-25

Dear Members,

I believe by this time at least some of the FCRA registered organisations would have started filing their FC-4 return for FY 2024-25. When I tried to file the return of an organisation, I found some difficulties in filing in the newly formatted FC-4 format.

For example, under the heading 2. Details of utilisation of FC, there are 5 sub headings to be filled. In 2.1 Utilisation, the normal details of (i) Utilisation for projects as per aims and objectives of the person/association (Rs.), ii) Total Administrative Expenses as provided in Rule 5, FCRR 2011 (Rs.) and iii)Total Foreigners as key functionary/working/associated are normally filled. In the i) we fill the details of project related expenditure and in the ii) we fill the administrative related expenditures. Below that there is (c) Foreign Contribution transferred to other persons/Associations before 29.09.2020 (The Foreign Contribution (Regulation) Amendment Act, 2020), which also can be filled if we have made any such transfers. Then comes D) Total utilisation in the year (Rs.) (A+C) that gives the correct amount utilised during the year for project and administrative expenses put together.

But, in the next sub-heading 2.2 Utilisation – Project wise, the columns Sl.No., Name of project/ activity, previous balance, receipt during the year, utilised and balance appear and in this the utilised column restricts us to the project expenses mentioned by us in the previous sheet. Only if we include the admin expenses also, the correct balance amount in the year appears, otherwise it is showing an incorrect balance, as it gets polluted automatically. If we change the figure in the previous sheet indicating the utilisation for projects, including the admin expenses, then the second sheet shows the correct balance, but in the previous sheet, the figure given as Total Utilisation in the year becomes wrong, as the admin expenses get added double time.

I feel the FCRA support team should do something to rectify this technical error. Or, if there is any other way to rectify this with the currently available format, it may please be indicated to us.

Yours sincerely,

Subramania Siva

Coimbatore, Tamil Nadu. - New Income Tax Bill 2025 provisions summarised for NPOs

Govt has brought out new Income Tax Bill 2025 to replace Income Tax Act 1961. While the overall Bill has a large number of provisions, SRRF has made a summary of impact of changes proposed in the new Bill for Non-Profit Organisations. These are summarised as below:

1. Consolidation and Simplification of Provisions

Unified Framework

a. The Bill consolidates scattered provisions related to NPOs into a dedicated chapter XVII Part B, covering clauses 332 to 355. The Chapter is further sub-divided into seven sub-parts. This will enhance clarity.

Standardized Terminology

b. “Registered Non-Profit Organisation or NPO” would be the new term encompassing entities registered under Sections 12A, 12AA, 12AB or 10(23C), provided their registration is not cancelled. This will replace existing term like Trust, Charitable, NGO, etc.

2. Streamlined Registration and Compliance

Existing Registrations

c. NPOs already registered under the current provisions need not re-register under the new bill. However new approvals under S.10(23C) will cease after 1-10-2024.

Structured Compliance

d. The bill introduces a structured approach to registration, taxation of income, permissible commercial activities, accumulation and compliance, etc.

3. Revised Income Computation mechanism

New Income Definitions

e. The bill introduces concepts such as ‘regular income’, ‘taxable regular income’, ‘deemed accumulated income’, and ‘residual income’ for NPOs. These definitions aim to provide a clearer framework for income computation.

f. Regular Income: consists of voluntary contributions consisting of general donations, rent from trust property, interest on trust funds, dividends from investments and income from incidental business activities. 85% application rule is generally calculated on regular income.

g. Taxable regular income: Regular Income that is not applied to charitable purposes and is not validly accumulated. Any regular income which is neither applied, nor validly accumulated, becomes taxable at 30%.

h. Residual Income: Total income of an NPO becomes fully taxable when the NPO violates certain core provisions of the Income Tax Act. These get triggered when an NPO

- Misapplies income (e.g. uses for non-charitable purposes),

- Engages in prohibited commercial activities (activities not incidental to main objects)

- Fails to maintain proper books of accounts

- Violates the terms of registration or approval

- Does not file income tax returns or audit report (Form 10B/10BB) within prescribed time.

- Fails to re-invest proceeds from asset transfers as required.

4. Major Changes in case of treatment of capital gains

Capital Gains Treatment: Earlier S.11(1A) allowed NPOs to claim exemption on capital gains if the net consideration from the sale of a capital asset was reinvested in acquiring another capital asset, as this reinvestment of income was treated as application for charitable purposes. However under the proposed Bill this option is no longer available and such gains are to be considered under the standard 85% application rule of regular income, as net consideration is considered part of regular income of an NPO. Thus there is no deduction available to NPOs for capital gains, otherwise covered under the Income Tax for other type of assessees.

5. Restrictions on Commercial Activities

The Income Tax Bill explicitly prohibits NPOs from engaging in any commercial activity, except for activities that are incidental to their objectives.

6. Section 80G revisions

Deductions for donations under S.80G are now covered under Clause S.133, under two clauses of 100% and 50%. Most NPOs would fall under the 50% category.

7. Introduction of the ‘Tax Year’ Concept

The bill updates the terms ‘assessment year’ and ‘previous year’ with ‘tax year’, aligning with international tax terminology.

8. Effective date

Govt has promised to bring the bill to come into effect on 1-4-2026.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Transfer of FCRA funds from the utilization account to the FCRA main account

Dear Sir/Madam,

I am writing here to get some clarity on FCRA funds.

One society is having 2 FCRA bank accounts one utilization account in PNB(This was the old receipt and utilization account) which is currently the deemed utilization account. After opening the FCRA SBI New Delhi Account, the society has not received any FCRA donations. The SBI account does not have any balance in it. Today the society received a email stating that the due to no transactions in the account it will be marked inoperative.

Can we transfer some funds from the PNB account to the SBI account which will be utilized at a later date for the societies activities only.

Thanks in advance,

Noel Gole - Use of FCRA funds remaining in FC accounts after FCRA certificate has been suspended / cancelled or deemed to Cease

MHA has come out with a clarification through a Public Notice dt 21-1-2025, that once a FCRA registration is suspended or cancelled, they cannot use FCRA funds lying either in Designated Bank account or Utilization bank Accounts. While in case of suspension / cancellation, FCRA authorities intimate SBI of the same, however no intimation goes to bankers who are maintaining Utilisation Accounts. Therefore, such bankers are not aware of the of suspension / cancellation of FCRA registration. At times, NPOs continue to use funds lying in these Utilisation bank accounts, even after FCRA has been suspended or cancelled. FCRA Dept has now clarified that such use is violative of FCRA provisions, and concerned NPOs could face penal action for the same.

The Dept has also clarified that any NPO, which fails to apply for renewal before expiry of registration, their FCRA registration falls under the category of Deem to be Ceased. Such NPOs cannot use FCRA funds lying in designated / utilization bank accounts after the registration has deemed to cease. Such NPOs who use fund after this date, are violating FCRA provisions, and could face penal actions.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Amendments in FC4 (wef 1-1-2025)

FCRA Form FC4 has been amended vide FCRA Amendment Rules 2024. These amendments are summarised below.

- Unspent Admin Expenses: If an entity has not spent allowable 20% of the FCRA funds received in a year, unspent part can be carried forward to next year. Thus say, an Association has received Rs 1 crore as FC receipts during FY 2024-25 and therefore at the maximum is allowed to spend Rs 20 lakh under Admin Heads. If it spends, say Rs 15 lakh only during FY 2024-25, new rules enable it to carry forward Rs 5 lakh to next year (FY 2025-26).

- Details of Chartered Accountant certifying FC4: Now details of chartered accountant who provides FC4 certificate are to be given in FC4. Details include Name, address, Member Registration No., Email address, Date of Issue of certificate, In case any violations pointed out then these need to be specified in the FC4.

- Chartered Accountant Certificate format amended: Now CA certificate needs to state that there are no violations, and in case there are violations, then these violations need to be specified.

- TDS refund rec’d in non-FCRA Bank A/c can be transferred to FCRA Bank A/c: FCRA authorities have vide Public Notice dt. 31/12/2024 have allowed to transfer any TDS refund received in non-FCRA account to be deposited in FCRA Bank a/c. In case the refund covers both FCRA deposits as well as non-FCRA deposits, than appropriate proportion of the same can be transferred to FCRA bank account from non-FCRA Bank account. FC4 has been suitably amended to disclose such refunds separately.

SRRF Dialogue Comment: Above changes reflect two major developments.

- By clarifying on TDS issue being deposited in non-FCRA Bank a/c, FCRA Dept for first time has shown some responsiveness to issues being raised by Associations. Hope there will be more such responsiveness by the Dept, on part of Associations, they should write more regularly to the Dept, wherever they face problems.

- On the line of Form 10B, FCRA Dept is also making Chartered Accountants specify that there are no violations, and if violations are there, these need to be specified. Thus the Dept forcing Chartered Accountants to be more accountable.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Two important notifications received from MHA

Regarding refund of TDS pertaining to foreign contribution received in non-FCRA bank account can be transferred to FCRA bank account…(click here for notification)

Administrative expenses can be carried forward to the next year…(click here for notification)

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - FCRA Validity extended to 31-03-2025

Validity of FCRA registration has been extended till 31-Mar-2025 vide a Public Notice issued by the FCRA (Director) on 27th December 2025. Thus all those NGOs whose FCRA had been earlier extended till 31-Dec-24 because their renewal application was pending with the FCRA Dept.

Also in case an NGO’s FCRA expires between 1st Jan 2025 and 31st March 2025 and they have applied for FCRA renewal before expiry of 5 year period from the date of previous FCRA registration, then their FCRA will also be extended to 30th June 2024.

In case renewal application is refused then the validity of the certificate shall be deemed to have expired on the date of refusal of application of renewal. In such a situation organization would not be eligible to either receive or utilize FCRA funds after such date.

Documents requirements made more stringent at the time of Renewal/Application

As per a press report all those applying for FCRA or renewing their FCRA would need to submit key documents like Memorandum of Association/Trust Deed, etc. Further now activity report has to be submitted for each-year and not a generic report, alongwith Accounts, including Receipt & Payment Account for each year.

—

Socio Research & Reform Foundation (NGO)

512 A, Deepshikha, 8 Rajendra Place,

New Delhi – 110008 - Is FCRA registration mandatory to invite foreigners as volunteers in a NPO?

Namaste Sir,

Greetings of the day!

We have been going through the blogs of Socio Research & Reform Foundation regarding FCRA.

We are Anatta Sangha Trust registered as a charitable public Trust under Indian Trusts Act 1882.

We want to invite foreign volunteers on an E3 Employment Visa to India (for honorary work with an NGO). So that they can work with us voluntarily in our projects for long term.

Kindly guide us whether FCRA registration is mandatory for our Trust to send them E3 visa invites along with our various registration documents. As of now, we don’t have FCRA registration.

We look forward to hearing from you.

Thanking You,

Warm Regards,

Sangha Das

Anatta Sangha Trust

Categories

-

Recent Posts

- Treatment of sale proceeds assets out of FCRA fund

- Latest Amendments in FCRA Rules & Forms – 3

- Latest Amendments in FCRA Rules & Forms – 2

- Latest Amendments in FCRA Rules & Forms -1

- Subscriptions to ZCZP Bonds to be allowed as CSR

- CSR spending during FY 2025

- FCRA 2026 put on hold

- Guidance Note on filing of FCRA Annual Return (FC-4)

- Show Cause Notice under Section 14(1) (e) of FCRA 2010

- Delhi HC rejects ‘one line refusal’ of FCRA Dept

Recent Comments

- Subhash Mittal on CSR spending during FY 2025

- George on CSR spending during FY 2025

- SRRF on Treatment of sale proceeds assets out of FCRA fund

- Subhash Mittal on Latest Amendments in FCRA Rules & Forms – 2

- Ravi Verma on Latest Amendments in FCRA Rules & Forms – 2

Web Pages

- Brief Profiles of Expert Panel members at SRRF Dialogue

- FC Forms

- FCRA Rules amended

- Galleries

- Happy New Year 2012

- Latest Post

- Salient Features of Multi-State Societies Registration Bill 2012

- Service Tax Notifications of Year 2012

- SRRF Advisory Series

- SRRF’S Webinar

- SSE in India

- Subscribe to SRRF Blog

Admin Area

Archives